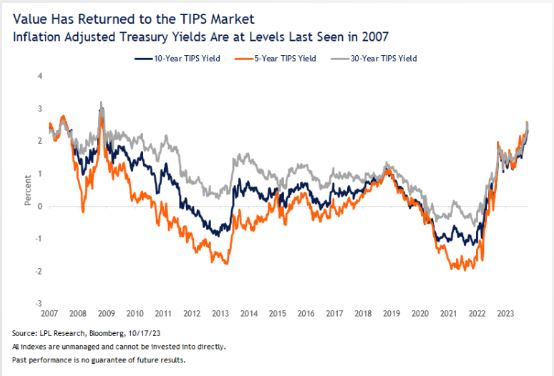

The move higher in Treasury yields (lower in price) has been unrelenting, with intermediate and longer term Treasury yields bearing the brunt of the move. Rates are moving higher alongside a U.S. economy that has continued to outperform expectations and not due to higher inflation fears. As such, the move higher has been largely driven by an increase in “real” yields, or inflation-adjusted yields or just TIPS (Treasury Inflation-Protected Securities).

TIPS are Treasury securities whose principal and interest payments are adjusted for inflation. Unlike other Treasury securities, where the principal is fixed, the principal of a TIPS can go up or down over its term. So, when the TIPS matures, if the principal is higher than the original principal amount, you get the increased amount. If the principal is equal to or lower than the original principal amount, you get the original amount. So, since these securities are government guaranteed, TIPS investors who hold the individual bonds to maturity receive, at a minimum, the original investment back plus coupons (paid semiannually) but could get more than the original investment if inflation surprises to the upside.

So, after spending years in negative territory, TIPS yields are decidedly positive again for 5-year, 10-year, and 30-year maturities and value has been restored in the TIPS market. Moreover, since 2007, TIPS yields have rarely been higher.

Looking at trailing returns, however, investors may be surprised to see the negative returns generated by the TIPS index (Bloomberg U.S. TIPS Index) despite generationally high inflationary pressures. The challenge for TIPS, has not been the inflationary environment (and thus the adjustment), but rather the aggressive rate hiking campaign by the Fed to arrest those high inflation pressures. And while TIPS provide a hedge against inflation, they do not provide a hedge against higher interest rates. So, with the Fed close to the end of its rate hiking campaign, the volatility experienced in TIPS over the last few years may be coming to an end as well. And with yields at levels last seen in over a decade, TIPS could provide an attractive real return for particularly those investors who can buy and hold individual bonds to maturity.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. For more information on the risks associated with the strategies and product types discussed please visit https://lplresearch.com/Risks

Treasury inflation-protected securities (TIPS) help eliminate inflation risk to your portfolio as the principal is adjusted semiannually for inflation based on the Consumer Price Index – while providing a real rate of return guaranteed by the U.S. Government.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Comments